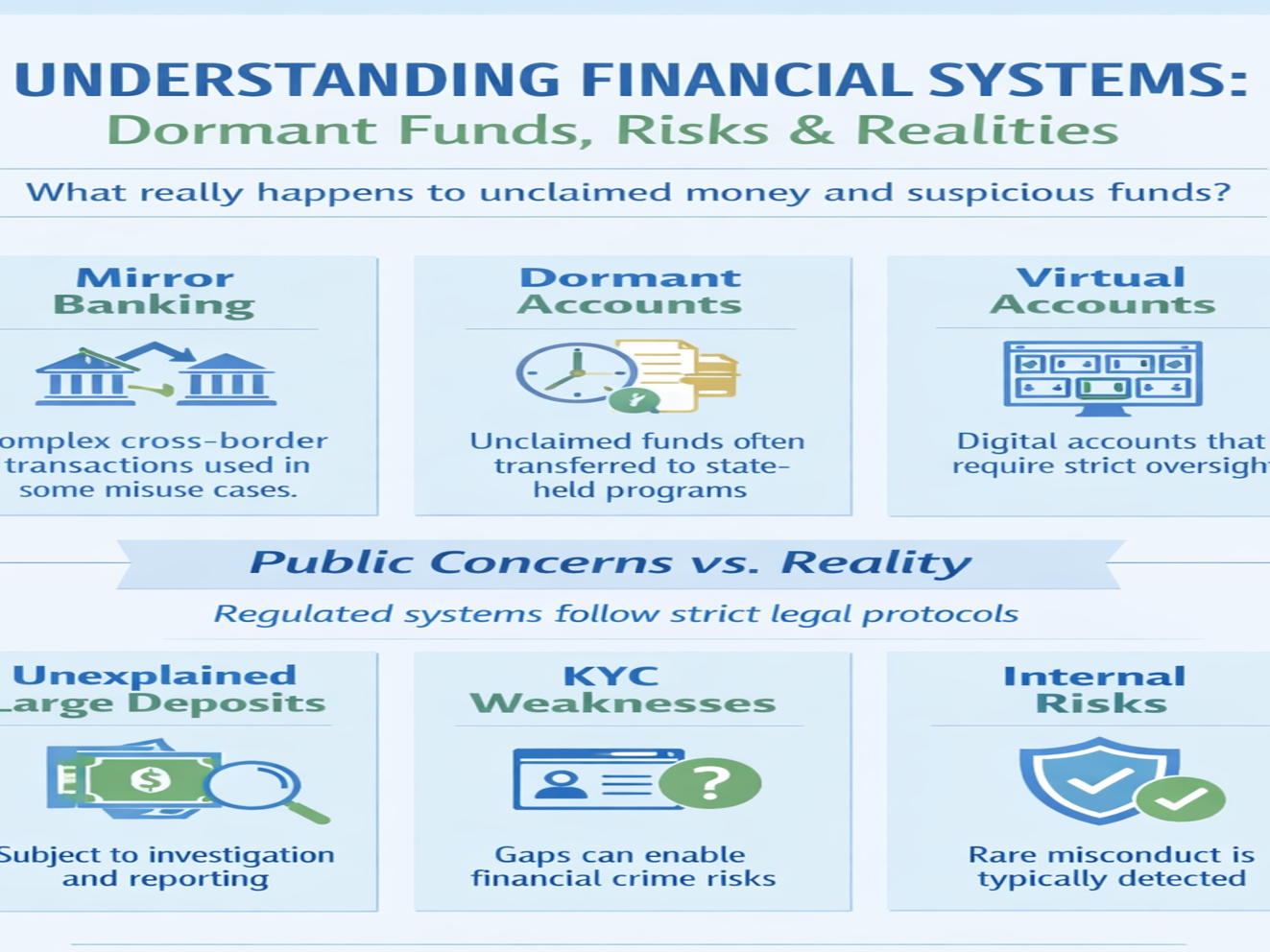

Understanding Financial System Risks: Dormant Funds, Compliance Gaps, and Public Misconceptions

Introduction: The Questions People Ask—And the Complexity Behind Them

Across many markets, there is a growing public curiosity—and at times, concern—about how banks handle certain categories of funds:

- Large unexplained deposits

- Dormant or unclaimed balances

- Digitally structured (virtual) accounts

- Cross-border transaction mechanisms

- Weaknesses in KYC (Know Your Customer) processes

In parallel, broader discussions around black money and money laundering continue to shape public perception.

Some of these concerns are valid. Others are driven by incomplete understanding.

This article does not attempt to accuse or expose. Instead, it aims to clarify, contextualize, and explain how modern banking systems are structured to deal with such situations—and where risks, in general terms, may exist.

1. The Global Context: Scale and Systemic Complexity

To understand the discussion, one must first appreciate the scale:

- It is widely estimated that $800 billion to $2 trillion is laundered globally each year (approximately 2–5% of global GDP).

- Industry studies suggest that less than 1% of illicit financial flows are intercepted.

- Dormant or unclaimed financial assets worldwide are estimated to exceed $100 billion.

- Financial institutions collectively spend over $200 billion annually on compliance, including AML (Anti-Money Laundering) and KYC systems.

These figures highlight one key reality:

The financial system is vast, highly regulated, and continuously evolving—but not entirely immune to risk.

2. Mirror Banking: Concept vs. Misuse

The term “mirror banking” has appeared in global discussions, often linked to cross-border fund movements.

Conceptual Understanding

In simplified terms, mirror-like structures may involve:

- Parallel transactions across jurisdictions

- Value transfer without direct physical movement of funds

Important Clarification

Such mechanisms, when used within regulated frameworks, can relate to legitimate financial structuring.

However, in certain globally documented instances, similar structures have been misused to:

- Bypass capital controls

- Obscure the origin of funds

Balanced View

It is important to note:

- This is not a standard retail banking function

- Any misuse is typically associated with regulatory gaps, weak oversight, or deliberate circumvention of controls

3. Dormant Accounts: What Happens to Unclaimed Money?

One of the most common areas of misunderstanding relates to dormant accounts.

What is a Dormant Account?

An account is generally classified as dormant after a prolonged period of inactivity (timeframes vary by jurisdiction).

Standard Industry Practice

In most regulated environments:

- Accounts are flagged and restricted

- Banks attempt to contact account holders

- Funds remain recorded under the customer’s ownership

In Case of Death

Funds are typically:

- Transferred to nominated beneficiaries, or

- Claimed by legal heirs through due process

If Funds Remain Unclaimed

In many jurisdictions:

- Funds are eventually transferred to state-managed unclaimed asset programs or central authorities

- These funds may be held for long-term claims or redirected into public-interest initiatives

Key Clarification

Banks do not have unrestricted rights to treat such funds as profit.

4. Virtual Accounts: Efficiency with Oversight Requirements

What Are Virtual Accounts?

Virtual accounts are digitally created sub-accounts linked to a primary account, commonly used for:

- Payment reconciliation

- Corporate collections

- Fintech integrations

Risk Consideration

While these are legitimate tools, like any financial mechanism, they require:

- Strong monitoring

- Transaction traceability

- Robust compliance oversight

Observed Challenges (Globally)

In certain international cases, complex transaction layering through digital channels has:

- Increased difficulty in tracking fund origins

- Required enhanced regulatory scrutiny

5. Large Unexplained Deposits: Regulatory Handling

A key concern often raised is how banks deal with significant deposits where the source of funds is unclear.

Regulatory Expectations

Banks are generally required to:

- Conduct enhanced due diligence

- Request supporting documentation

- Monitor account activity

- Report suspicious transactions to relevant authorities

Possible Outcomes

Depending on the case:

- Transactions may be restricted

- Accounts may be monitored or temporarily frozen

- Reports may be filed with financial intelligence units

Clarification

There is often public speculation regarding how such funds are treated. However, within regulated systems:

Banks operate as custodians and are required to follow strict legal processes—they do not have discretionary authority to reallocate such funds for their own use.

6. KYC (Know Your Customer): The First Line of Defense

KYC remains a foundational element of financial integrity.

Purpose

- Verify identity

- Assess risk

- Prevent misuse of the financial system

Where Challenges Arise

Globally observed issues include:

- Use of falsified identities

- Shell entities with limited transparency

- Outdated verification processes

- Human error or procedural gaps

Implication

Weaknesses in KYC frameworks can:

- Increase exposure to financial crime

- Require stronger regulatory intervention

7. Black Money and Money Laundering: Structural Overview

Money laundering is typically understood in three stages:

1. Placement

Introducing illicit funds into the system

2. Layering

Creating complex transaction trails to obscure origin

3. Integration

Reintroducing funds as apparently legitimate assets

Role of Financial Institutions

Banks:

- Serve as intermediaries in financial flows

- Are subject to strict compliance obligations

- Are expected to detect and report irregularities

Important Perspective

The presence of financial crime does not necessarily indicate institutional intent—but highlights the need for continuous system strengthening.

8. Internal Risks: A Balanced and Realistic View

A question that occasionally arises is whether internal actors within financial institutions could misuse such systems.

Structural Safeguards

Modern banking systems typically include:

- Multi-level authorization processes

- Automated transaction logs

- Internal audit functions

- External regulatory audits

Reality Check

While no system is entirely immune to risk:

- Globally documented cases of internal misconduct are rare and typically isolated

- Such cases are usually:

- Detected through audit systems

- Subject to strict legal consequences

Balanced Conclusion

System design significantly limits the possibility of systematic misuse, though continuous vigilance remains essential.

9. What Actually Happens to “Grey Zone” Funds?

To simplify:

Scenario-Based Outcomes

- Legitimate but undocumented funds

→ Held pending clarification - Suspicious transactions

→ Reported and monitored - Confirmed illegal funds

→ Subject to legal seizure processes - Dormant/unclaimed funds

→ Transferred according to regulatory frameworks

10. Why Public Perception Differs from Reality

There are three key drivers:

1. Complexity

Financial systems are not easily visible or understood

2. High-Profile Global Cases

Isolated incidents shape broader perception

3. Information Gap

Customers rarely see internal compliance processes

11. The Real Risk: System Gaps, Not System Intent

The most significant risks in global finance are not necessarily rooted in intent, but in:

- Regulatory inconsistencies across jurisdictions

- Technological gaps

- Rapid financial innovation

- Cross-border complexity

Conclusion: Moving from Suspicion to Understanding

The modern banking system operates within a dense framework of:

- Regulation

- Compliance

- Oversight

- Accountability

While risks exist—and must be acknowledged—the narrative that financial institutions systematically misuse customer funds is not supported by how regulated systems are designed to function.

A more constructive question is:

How do we continue strengthening financial systems to reduce misuse, improve transparency, and build public trust?

That is where meaningful progress lies.

Disclaimer

This article has been authored and published in good faith by Dr. Dharshana Weerakoon, DBA (USA), based on publicly available global financial data, established regulatory frameworks, widely recognized industry practices, and professional experience across international markets.

The content is intended solely for educational, analytical, and public awareness purposes to encourage informed discussion on financial systems, banking governance, compliance structures, and risk management.

All references are generalized, illustrative, and non-specific, and do not refer to or imply any particular institution, organization, individual, or jurisdiction. The author does not make or intend any allegation or assertion of wrongdoing against any entity.

This article does not constitute legal, financial, or investment advice. Readers are encouraged to seek professional guidance for specific matters.

The views expressed are personal, independent, and analytical, and are presented in alignment with applicable legal, ethical, and professional standards.

Further Reading: https://www.linkedin.com/newsletters/outside-of-education-7046073343568977920/

Further Reading: https://dharshanaweerakoon.com/a-time-for-strategic-reflection/