The Paradox of Digital Efficiency and Paper Chaos in Sri Lankan Banking

Introduction

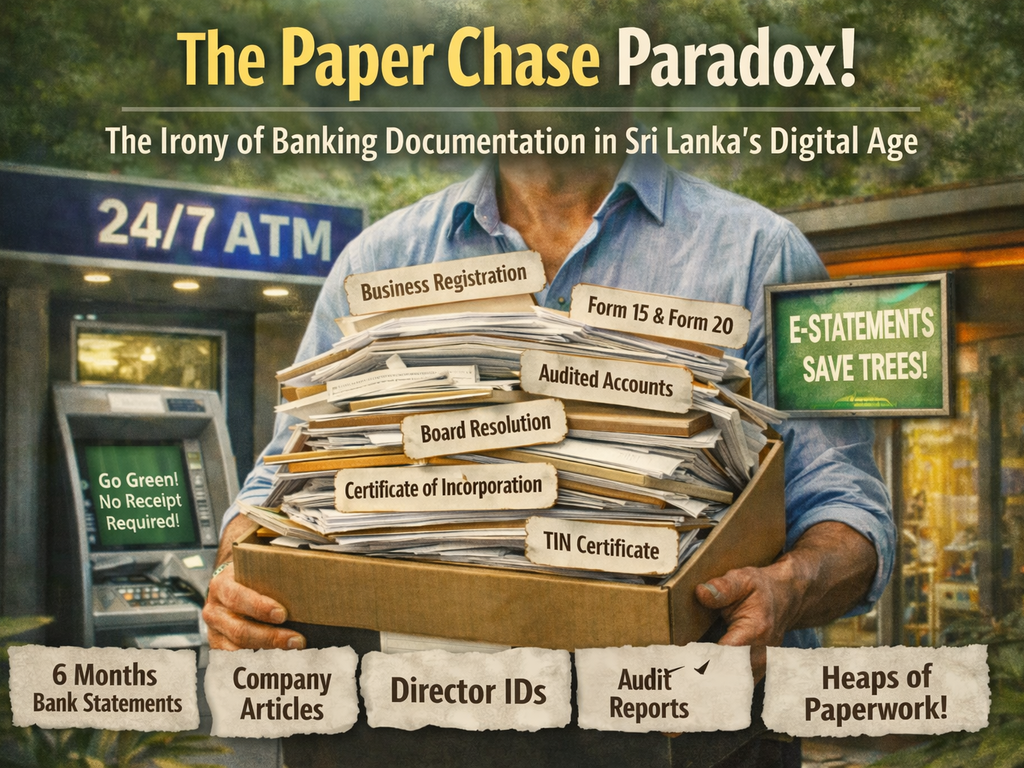

In an era where technology promises efficiency and sustainability, Sri Lankan banks offer a curious paradox. On one hand, ATMs operate 24/7, air-conditioned and well-lit, prompting users to “save trees” by skipping printed receipts. Banks also encourage e-statements, reducing stationery costs and environmental impact. Yet, when it comes to opening a bank account or obtaining financial facilities, customers are asked to submit reams of paper documents, often spanning multiple months. This disconnect between digital efficiency and bureaucratic paper practices highlights a gap between modern banking innovation and administrative tradition.

This article presents an analytical and educational perspective based on publicly available information, professional experience, and Sri Lanka’s legal framework for digital documents. It is intended to inform, stimulate discussion, and promote sustainable banking practices.

The Digital Efficiency Narrative

Modern banking in Sri Lanka is evolving rapidly. ATMs have become the frontline of digital convenience. These machines, equipped with air-conditioning and energy-efficient LED bulbs, allow customers to access cash at any hour. During withdrawals, users are asked whether they require a receipt—an initiative aimed at reducing paper consumption. A simple instruction on the receipt reminds: “Please consider the environment before printing.”

Additionally, banks increasingly issue e-statements rather than printed ones. According to publicly available Central Bank reports, over 70% of corporate customers and 55% of individual clients now opt for digital statements. This shift saves millions of A4 sheets annually and reduces costs by an estimated LKR 250 million across the banking sector. The adoption of digital banking platforms has grown by 42% in the past five years, reflecting a global trend toward efficient, secure, and environmentally conscious banking.

The push toward digital efficiency also extends to mobile banking apps, online transfers, and real-time account monitoring. These platforms reduce operational delays and improve cash flow management.

The Paperwork Paradox

Despite these innovations, the paradox emerges when engaging in banking processes like account opening, loan applications, or trade finance. Businesses are often asked to submit:

- Certified copies of the incorporation certificate (business registration) and articles of association.

- Form 15 & Form 20, and directors’ national identity cards.

- TIN certificates and official applications.

- Last six months’ printed bank statements from other financial institutions.

- Audited financial statements and board resolutions on official letterhead.

While intended for regulatory compliance, the volume of paperwork creates operational inefficiency, delaying business operations and causing frustration. SMEs often spend upwards of 40 hours compiling documents, reducing productivity.

Legal Recognition of Digital Documents

Sri Lanka legally recognizes digital documents and electronic signatures under the Electronic Transactions Act No. 19 of 2006 (amended by Act No. 25 of 2017). Key provisions include:

- Electronic documents are legally valid: No electronic record or data message shall be denied legal effect solely because it is in electronic form.

- Electronic signatures are recognized: Reliable electronic signatures satisfy legal requirements for signing documents, provided they can identify the signer and demonstrate the document was not altered after signing.

- Paperless compliance: Banks and businesses can accept electronically signed documents for corporate transactions, reducing the need for physical paperwork.

This means that incorporation certificates, audited accounts, board resolutions, and other corporate documents can be submitted digitally, as long as they meet reliability and security standards defined by law.

🧠 Important Clarification: Simple scanned copies or pasted images of signatures do not qualify as legally valid digital signatures. Authentic electronic signatures must meet the reliability and verification requirements under Sri Lankan law.

Case Studies: Bureaucracy vs. Digital Efficiency (Illustrative & Anonymized)

- Tea Exporter, Nuwara Eliya – Required 12 documents totaling over 100 A4 pages to open a corporate account. Process extended four weeks.

- Tourism Startup, Colombo – Six months of printed statements from three separate accounts delayed project launch by two months.

- Hospitality Group, Kandy – Loan approval delayed due to missing board resolutions on official letterhead.

- Small Guesthouse, Galle – Notarized handwritten forms were required, despite ATM eco-friendly receipts.

- IT Solutions Company, Colombo – Auditors required physical copies of all financial documents.

- Adventure Tourism Operator, Ella – Delayed operational financing due to physical submission requirements.

- Agri-Tourism Venture, Matale – Compliance slowed loan approvals.

- Luxury Hotel, Negombo – Multi-currency account setup delayed six weeks due to repeated document requests.

- Boutique Eco-Resort, Haputale – Physical submission of environmental compliance certificates required despite electronic copies.

- Travel Agency, Colombo – Trade credit facility delayed by insistence on paper-based board resolutions.

These examples are anonymized, illustrative, and highlight the gap between current bureaucratic practices and the legal recognition of digital documents.

Economic and Environmental Implications

Economic Implications:

- Project delays affecting revenue and employment.

- Increased administrative costs.

- Potential deterrent to foreign investors.

Environmental Implications:

- Mandatory submission of A4 sheets undermines sustainability.

- Estimated 1.2 million sheets consumed annually for compliance.

- Additional carbon footprint from printing, couriering, and storage.

Modernizing compliance to align with digital transactions could significantly reduce this footprint.

Comparative Global Practices

- Singapore: Digital onboarding using secure e-KYC systems reduces paper documentation by 90%.

- United Kingdom: Fully digital board resolutions and audited accounts accepted electronically.

- India: E-signatures and digital certificates are legally recognized.

- Australia: Cloud-based corporate document storage ensures accessibility without printing.

Sri Lanka can adopt similar frameworks to reduce administrative burdens while maintaining regulatory compliance.

Recommendations for Sustainable Banking Practices

- Digital Compliance Integration: Implement e-forms for account openings and loan applications.

- E-Authentication of Documents: Adopt secure portals for verifying digital signatures.

- Policy Harmonization: Align regulatory guidelines with digital banking.

- Customer Education: Promote eco-friendly banking practices and digital literacy.

- Incremental Rollout: Pilot fully digital account openings, tracking efficiency and environmental impact.

- Sector Collaboration: Work with tourism and hospitality associations to identify bottlenecks.

- Sustainability Metrics: Introduce KPIs for paper reduction and cost savings.

Tourism & Hospitality Lens

Tourism operators are directly affected by banking delays. Seasonal revenue cycles mean loan or account approval delays impact staffing, vendor payments, and promotions. Streamlining digital compliance supports operational efficiency and aligns with sustainability principles.

Policy Implications and Strategic Insights

Policymakers and regulators could:

- Recognize legal validity of digital documents.

- Incentivize banks to adopt paperless onboarding.

- Monitor environmental impact metrics.

- Collaborate with industry stakeholders for user-friendly frameworks.

Such initiatives improve efficiency, sustainability, and investor confidence.

Conclusion

Sri Lanka’s banks exhibit a duality: digital, eco-conscious transactions coexist with paper-heavy compliance protocols. Leveraging the legal recognition of digital documents can bridge this gap, enhancing efficiency, supporting economic growth, and reinforcing environmental responsibility. By harmonizing digital innovation with regulatory rigor, Sri Lanka can model sustainable banking in the 21st century.

Disclaimer

This article has been authored and published in good faith by Dr. Dharshana Weerakoon, DBA (USA), based on publicly available information, professional experience, and legal provisions under Sri Lankan law. It is intended solely for educational, journalistic, and public awareness purposes. The author accepts no responsibility for misinterpretation or misuse. Views are personal and analytical, and do not constitute legal, financial, or investment advice. All case studies are anonymized and illustrative. This article complies with Sri Lankan law, including the Electronic Transactions Act No. 19 of 2006 (and amendments), the Intellectual Property Act No. 52 of 1979, the ICCPR Act No. 56 of 2007, and relevant data privacy and ethical standards. ✍ Authored independently and organically through professional expertise—not AI-generated.

Further Reading: https://www.linkedin.com/newsletters/7046073343568977920/

Further Reading: https://dharshanaweerakoon.com/are-sri-lankan-entrepreneurs-working-for-banks/